Brussels / Strasbourg — The European Commission on Wednesday, June 3, 2026, unveiled a long-awaited “technological sovereignty” package aimed at rebuilding Europe’s industrial capacity in artificial intelligence, semiconductors, cloud computing, and open source — the most concrete legislative answer yet to years of warnings that the bloc has become structurally dependent on US hyperscalers.

The package is structured as four interlocking pieces: two legislative proposals — the Chips Act 2.0 and the Cloud and AI Development Act (CADA) — alongside two supporting strategies: an EU Open Source Strategy and a Strategic Roadmap for Digitalisation and AI in the Energy Sector. The legislative texts will now go through the European Parliament and the Council, where unanimous approval from all 27 member states is required.

Why now: the bill for US cloud

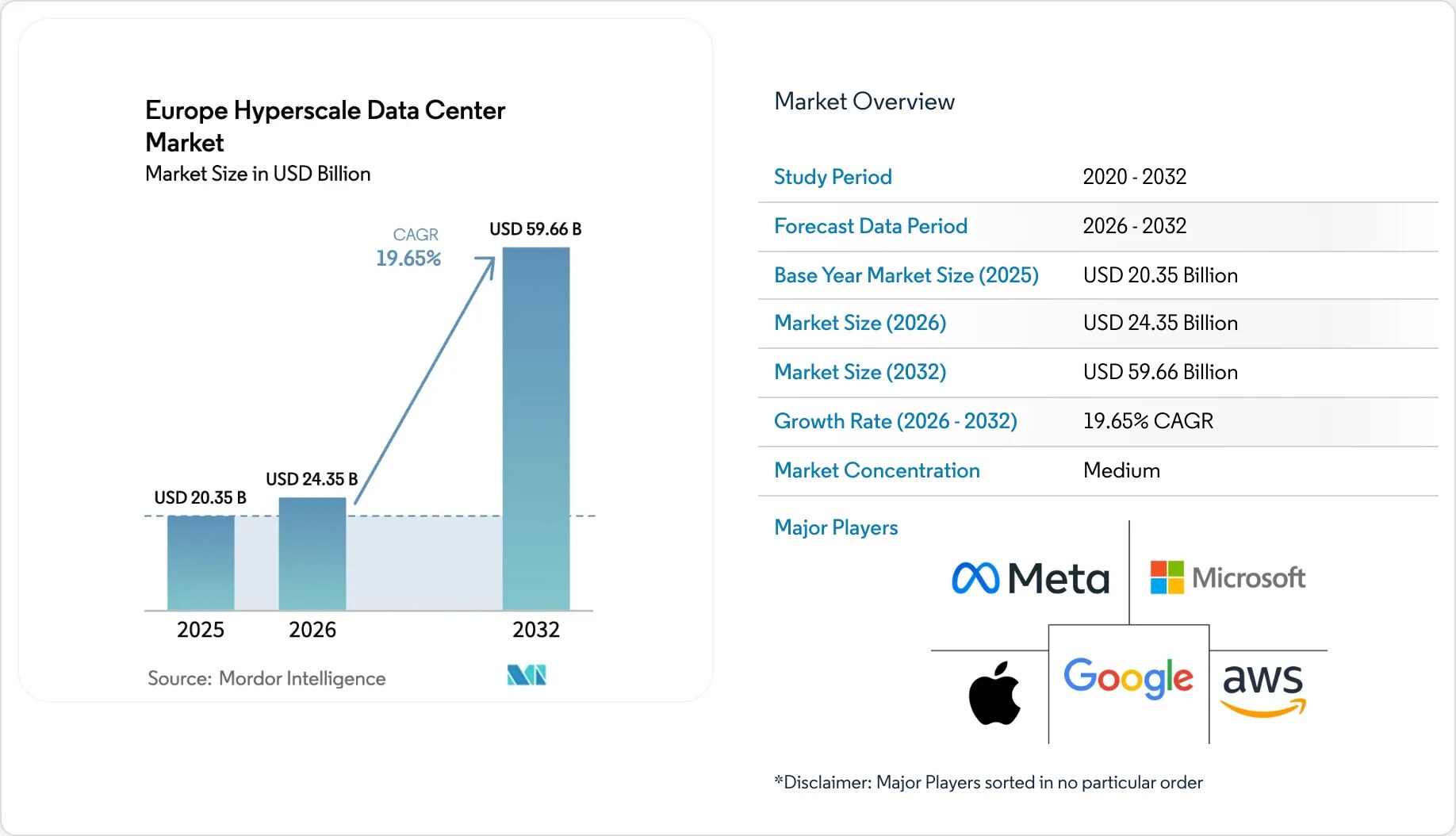

Brussels has grown increasingly blunt about the cost of doing nothing. The Commission estimates the EU spends hundreds of billions of euros a year on US cloud software services, and that American hyperscalers — Amazon Web Services, Google Cloud, and Microsoft Azure — control more than 65% of the European cloud market. That structural exposure has gone from a procurement concern to a sovereignty flashpoint, sharpened by export-control disputes, transatlantic sanctions frictions, and a string of high-profile “switch-off” incidents in which US providers revoked service to European public bodies.

Chips Act 2.0: from 2023 framework to first-of-a-kind fab

The Chips Act 2.0 updates the 2023 European Chips Act and explicitly targets the segments the original framework under-weighted: AI chips and AI accelerators, advanced process nodes, chiplet integration, advanced 3D packaging, and photonic integrated circuits. A flagship commitment in the new text is a first European facility combining leading-edge node manufacturing, chiplet integration, and 3D advanced packaging under one roof, with trial production planned for 2030–2033.

A new third semiconductor IPCEI (Important Project of Common European Interest) candidate pipeline has been scoped, naming AI chips and accelerators, photonic ICs, heterogeneous integration, advanced packaging, sensors, power semiconductors, and secure communication chips as priority tracks.

Notably, the Commission declined to attach a specific euro figure to the package. Funding for the 2028–2034 period will be set in the next Multiannual Financial Framework (MFF) negotiations — a delay that has already drawn criticism from industry groups who argue the package is “directionally right, financially vague.”

CADA: a sovereign cloud and AI stack

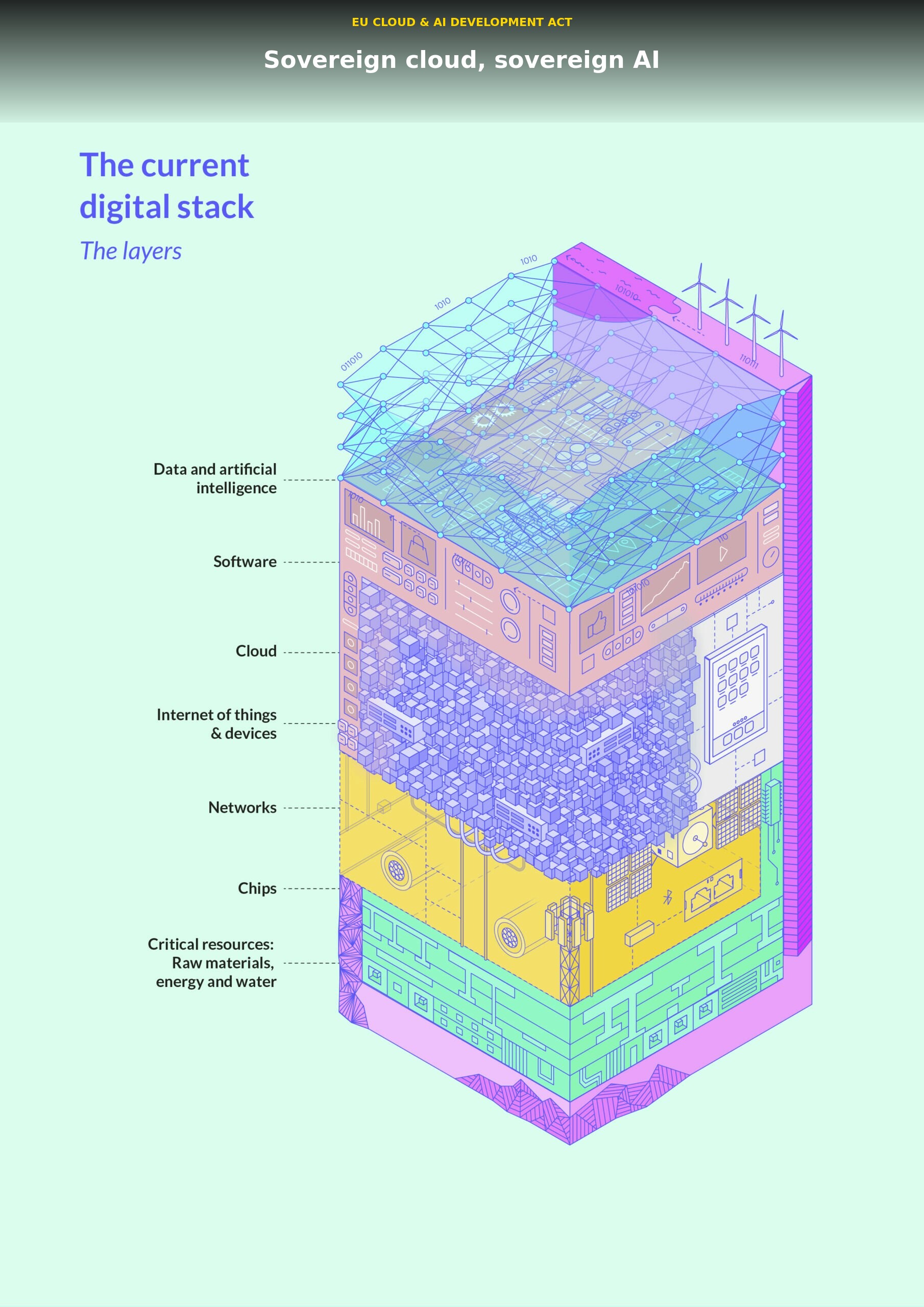

The Cloud and AI Development Act (CADA) is the more novel of the two bills. Its two main objectives are to strengthen the EU’s cloud and AI ecosystem and to bolster Europe’s leadership in high-performance computing resources and digital infrastructure for AI development. The Commission has positioned CADA as the demand-side counterpart to Chips Act 2.0’s supply-side push — building the compute, storage, and orchestration layer on top of the silicon.

A RAND Europe evidence response published in 2025 had already warned that, even with CADA in force, Europe’s AI compute gap will not close on legislation alone — the underlying infrastructure investments and skill base have to scale in parallel.

The industry is not waiting for Brussels

While the package was being drafted, the EuroStack Industry Group had already moved. On 14 March 2025, the European DIGITAL SME Alliance helped assemble an open letter signed by nearly 100 industry leaders urging decisive action; by 6 May 2025, a second open letter — “Buy, Sell and Fund European!” — went to Commission President Ursula von der Leyen, Executive Vice-President Henna Virkkunen, and other senior officials, with the coalition now over 200 signatories strong.

“Urgency is an understatement — Europe must act swiftly to safeguard its digital sovereignty. Every day of delay in making critical decisions and taking decisive action brings us closer to complete dependence on non-EU digital technologies. We have the talent and resources; what we need is a framework that accelerates progress.”

— Andrei Kelemen, CEO, Cluj IT Cluster

The EuroStack report, authored by Francesca Bria, has become a reference document for the Commission’s framing. Signatories include open-source firms such as Nextcloud and a broad coalition of European cloud, semiconductor, and industrial-tech players.

The hyperscaler fightback

Not everyone is on board. A EuroStack analysis published earlier this year warned of a “surprising new alliance between traditional industry and hyperscalers” lobbying to soften or redirect the package — particularly the “Buy European” provisions that would direct public procurement and subsidies toward sovereign-grade cloud and chip vendors. The Commission will have to balance that pressure against the demands of its own industrial constituency.

France-Germany axis: sovereign cloud, ahead of Brussels

The package also formalises a bilateral track that started a year ago. On 1 September 2025, France and Germany launched a coordinated strategy to reinforce European digital sovereignty, including a sovereign cloud initiative that pre-figures several of CADA’s provisions. Paris and Berlin have effectively used the bilateral channel to set the political tone for the EU-wide package.

What’s next

The legislative clock now takes over. The Chips Act 2.0 and CADA will be negotiated in parallel through the European Parliament and the Council. Expect:

- Late 2026 / early 2027: Council common position and Parliament rapporteur reports.

- 2027: Trialogue negotiations; risk of dilution on procurement and IPCEI scope.

- 2028–2034: Funding window, gated on the next MFF deal — the make-or-break variable.

- 2030–2033: Trial production at the planned advanced-node + chiplet + 3D packaging facility.

For the EU, the package is the most ambitious bet yet that industrial policy, not just regulation, is what closes the sovereignty gap. Whether €multi-billion translates into deployed capacity before the next crisis hits is the question that will define Europe’s digital decade.

Sources: European Commission press corner (IP/26/1187); European DIGITAL SME Alliance; EuroStack Industry Group open letters (March & May 2025); RAND Europe evidence response on CADA; Mordor Intelligence; Xinhua; CNBC; Cluj IT Cluster; Bertelsmann Stiftung.